As the European Payments Initiative activates e-commerce acceptance, merchants must navigate the precarious friction between geopolitical resilience, working capital optimization, and checkout conversion rates.

The infrastructure underpinning European commerce is undergoing its most significant structural shift since the decoupling of domestic networks. In France, Groupe BPCE — acting as a principal driver of the European Payments Initiative (EPI) — has initiated the commercial rollout of Wero for e-commerce via its acquiring subsidiary, Payplug.

For retail executive boards, Chief Information Officers, and treasury leads, this is not a cosmetic iteration of legacy initiatives like Paylib. It represents a fundamental architectural pivot that forces merchants to arbitrate between a highly strategic political mandate — sovereignty — and day-to-day operational conversion efficiency.

1. Stripping the Network Layer: The Pure-Play A2A Architecture

At its core, Wero relies on a radical structural simplification: the complete elimination of the traditional card network layer in favor of SEPA Instant Credit Transfer (SCT Inst) rails. It is an account-to-account (A2A) “push” mechanism. It operates entirely independently of card schemes, card-bound digital wallets, or alternative cryptographic tokens.

This architectural variance alters the fundamental velocity of liquidity. Transactions settle with total finality in under 10 seconds, operating 24/7/365. For high-volume enterprise retailers, this compressed clearing cycle shifts settlement from standard T+1 or T+2 card processing delays to real-time cash availability. For a merchant capturing €1M per week in transaction volume, migrating that volume to Wero yields an immediate, recurring working capital improvement of €2M to €3M.

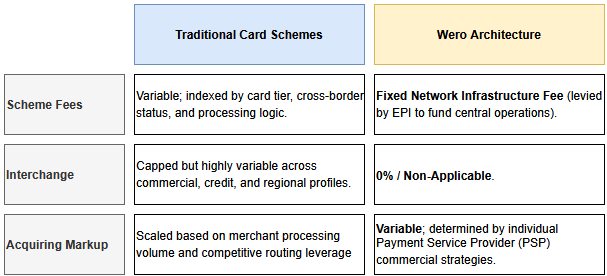

2. The Economics of the Merchant Service Charge (MSC)

By bypassing card networks, Wero structurally dismantles the cost stack typical of the four-party model:

The Commercial Reality Check

Early access pilot data indicates that commercial merchant pricing sits between 2.0% and 3.0% — putting it on par with alternative wallets like PayPal, but making it significantly more expensive than highly optimized domestic debit networks, such as France’s Groupement Carte Bancaire (CB). Accepting “pricing to be determined at a later date” contractually exposes early adopters to severe post-launch margin compression.

3. The Redirection Friction: Balancing Conversion Against Cost

While the financial settlement layer favors the merchant, the frontend user experience introduces material friction. Unlike tokenized, one-click card-on-file checkouts or native device authentication (e.g., Apple Pay), Wero currently utilizes an App-to-App redirection protocol to the consumer’s mobile banking interface.

In conversion-critical digital retail environments, redirection is a known drop-off point. Because Wero lacks immediate consumer brand equity outside its initial launch geographies, merchants face an increased risk of cart abandonment at the checkout stage. Currently, there are no published benchmark conversion datasets comparing Wero directly against premium tokenized card flows.

Furthermore, the domestic market landscape in France remains deeply entrenched:

- Carte Bancaire (CB): Controls ~70% of e-commerce transaction volumes.

- PayPal: Captures ~15–20%.

- Google Pay / Apple Pay: Captures ~5–10% and exhibits accelerating growth.

- Legacy SEPA / Standard Bank Transfers: Represents ~2–5%.

To secure meaningful market share, Wero cannot rely solely on infrastructure cost benefits or political sovereignty talking points. It must actively convert consumers who currently encounter zero friction using biometric card wallets.

4. Operational Blind Spots: Irrevocability, Fraud, and Litigations

Enterprise implementation teams must audit three critical gray areas before dedicating resources to Wero integration:

The Accounting Nightmare of Real-Time Irrevocability

Under the card scheme model, transactions can be voided or reversed before final end-of-day clearing. Because SCT Inst transfers are instantly final and irrevocable upon execution, authorization reversals do not exist within the Wero network. Any post-settlement funds return requires a completely separate, standalone transaction — a credit transfer from the merchant’s account to the consumer. This creates decoupled reconciliation line items that legacy Order Management Systems (OMS) and ERP platforms must be manually reconfigured to handle.

Unvalidated Feature Parity

Wero’s architectural specifications technically account for advanced payment primitives, specifically Merchant Initiated Transactions (MIT) for subscription billing and authorization holds for pay-on-delivery use cases. However, these remain unvalidated in scaled production environments. Retailers must maintain robust card-based fallback systems to protect recurring revenue streams.

Immature Dispute and Chargeback Frameworks

The protection mechanisms and chargeback allocation rubrics that govern automated consumer disputes are not yet fully operational. During transitional co-branding phases — such as the Dutch market migration where iDEAL and Wero will run simultaneously from 2026 to late 2027 — merchants will be forced to support two entirely separate dispute operating procedures simultaneously.

The Liability Shift Catch-22

Wero documentation promises a full liability shift for fraud from the merchant to the issuing bank, contingent upon Strong Customer Authentication (SCA) via biometric verification inside the banking application. However, if an issuing bank permits an authentication exemption or down-grades the SCA flow, the fraud liability immediately reverts to the merchant.

5. Strategic Playbook for Enterprise Retailers

Wero cannot be treated as a localized payment option; it is an active market replacement play. In Luxembourg, Payconiq faces a definitive sunset by September 30, 2026. In the Netherlands, iDEAL will be fully phased out by the end of 2027. Cross-border merchants operating in these jurisdictions face a mandatory transition: integrate Wero, or lose domestic market access entirely.

For French retailers where integration remains an option rather than a mandate, the following actions are critical:

- Quantify Forced Cross-Border Exposure: Immediately calculate the transaction volumes currently routed through iDEAL and Payconiq. Model the financial impact of a conservative 10–20% cart abandonment rate during the initial migration windows.

- Enforce Acquirer Transparency: Do not sign processing agreements that leave commercial pricing open-ended. Demand fully documented Merchant Service Charge breakdowns, and negotiate tiered volume discounts before committing technical resources.

- Map POS Hardware Lifecycles: Wero’s point-of-sale (POS) terminal integration is scheduled for 2027 and beyond, with a heavy emphasis on dynamic QR codes. Because European in-store retail infrastructure is overwhelmingly optimized for Near-Field Communication (NFC) “Tap-and-Go” gestures, forcing a shift to QR code scanning presents severe localized checkout friction. Retailers must begin auditing their terminal fleets to ensure hardware capability for 2027/2028 deployments.

Let’s Drive the Conversation Forward

Sovereign payment rails are changing the balance of power between traditional international card schemes and domestic merchant ecosystems. However, a successful deployment requires looking past the political positioning to rigorously audit the underlying technical realities — from the complexities of instant ledger reconciliation to the fine print of fraud liability transfer.

At ITOPYX, we partner with enterprise retail organizations, CFOs, and technology leaders to architect resilient, agile, and cost-optimized payment ecosystems. We provide unbiased, infrastructure-level strategic advisory services designed to keep treasury independent, transaction costs minimized, and checkout conversion flawless.

How is your organization mitigating the operational risks of the SEPA Instant transition? Let’s connect to discuss your payment challenges, orchestrate your routing architecture, and future-proof your checkout stack.

ITOPYX

ITOPYX